Creo que no me equivoco si afirmo, aunque cueste creerlo, que las

elecciones en Cataluña están generando más atención

entre los inversores internacionales que las del Gobierno de España

celebradas hace un año, cuando estaba claro que ganaría Rajoy por

mayoría absoluta.

Ya percibí esa sensación la semana pasada en Londres. Les preocupa

una posible victoria contundente de CIU que desemboque en el inicio de

un proceso de separación. Y lo que podría suponer no

sólo para España, sino para toda Europa.

Por ejemplo, Virginie Maissonave, gestora de renta

variable global de Schroders, lo veía un riesgo muy

importante para toda la zona euro y dice que era uno de los

motivos por los que no tenía acciones de España y otros países en

cartera: "Me preocupa mucho la separación de Cataluña,

contagiaría otras regiones... Enorme inestabilidad en Europa"

La banca de inversión internacional también está haciendo sus

cábalas. Esta mañana me ha llegado un informe de Credit

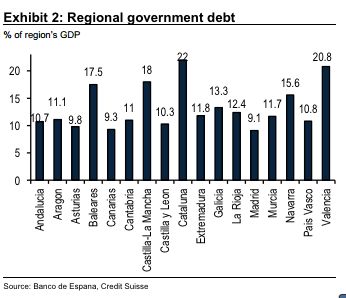

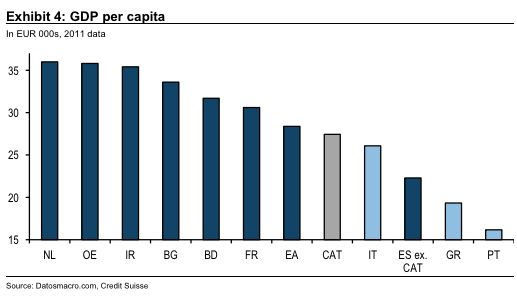

Suisse. Hace hincapié en que es la región más endeudada de España,

pero también la más rica, como se demuestra en este gráfico, con el

PIB per cápita, que demuestra que España se quedaría como un país con

menor PIB per capita que Cataluña si ésta fuera independiente:

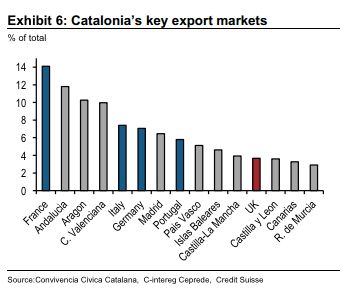

Pero que también tiene una elevada dependencia de España para sus negocios.

Copio a continuación las conclusiones en inglés, pero las resumo antes:

- "El objetivo de Mas es un pacto fiscal más que la

independencia desde nuestro punto de vista"

- "Una mayoría absoluta reforzaría la posición negociadora de

Mas. Podría conseguir más concesiones utilizando de modo más

contundente el argumento de la indepencia".

- Si hay independencia, incluso si hay negociaciones y "Cataluña

se queda en el euro y no crea una nueva moneda, los bancos catalanes

no tendrían acceso al Banco Central Europeo y no habría protección del

ESM para esta endeudad región. Por lo tanto vemos extremadamente

improbable que CAtaluña eliga la opción extrema de declarar

unilateralmente la independencia"

- "Pero los mercados financieros podrían seguir trabajando con

el ruido secesionista mientras Mas continue intentando obtener

concesiones fiscales de Madrid después de las elecciones"

Aquí los extractos de las conclusiones de Credit Suisse:

But financial markets might need to continue putting up with

secessionist noise as Mas

tries to extract fiscal concessions out of Madrid following the election.

Fiscal austerity is at the root of the call for early elections

and also at the root of the

more secessionist fervour. Voters feel they would be better off

if they were not part of

Spain and that has prompted a surge in national sentiment and

anger at Madrid’s

perceived power grab.

Mas’ goal is a fiscal pact rather than independence in our view.

He has long sought to

re-negotiate intra-regional transfers and for Catalonia to be

able to set up its own tax

agency along the lines of Navarre and the Basque country.

Behind his call for

independence is thus political opportunism and he has already

expressed frustration that

the central government in Madrid is not offering to negotiate

given his call for a referendum.

An absolute majority for the CiU would strengthen Mas’ hand

when. He could then

attempt to get more concessions by using the independence card

more strongly. The most

recent opinion polls, however, indicate that he might fall short

of securing the absolute

majority, but there is still a large, nearly one-third, of

undecided voters.

Madrid is also playing a game of brinkmanship. With Catalonia

being the most

indebted of Spain’s regions and Catalonia fully depending on

Madrid to finance this debt

Madrid feels that it does not need to make concessions in a

hurry. Increased transfers to

Catalonia might be in the pipeline, however. The financing

system of the autonomous

regions is reviewed every five years. The last revision was done

in 2009 so the next one is

not due until 2014. But the government has already stated that

it would bring the review

forward into next year. As in 2009, when Catalonia got a larger

share of taxes raised in the

region a further increase should not be excluded. Increased

transfers could deflate some

of the nationalist zeal.

A reform of the financing of the regions which could bring about

a more federal system is

required in the view of some of the Madrid government’s

politicians. But such a reform is

unlikely to be attempted in the current legislature with the

government’s hands full trying to

comply with deficit targets and implementing an array of

structural reforms to make

Spain’s debt more sustainable and the economy more flexible and competitive.

Secession is strongly opposed by the conservative government in

Madrid. All legal

levers will be used to prevent a referendum. Should Catalonia

persevere, the extreme

case would be an illegal consultation followed by a unilateral

declaration of independence.

But given the economic costs resulting from remaining outside

the EU and euro area a

‘yes’ to independence should not be a foregone conclusion. And

even if Catalonia would

hold on to the euro and not create a new currency from the

outset, Catalonian banks

would not have access to the ECB and there would be no

protection from the ESM for this

highly indebted region. It is thus extremely unlikely that

Catalonia choses the extreme

option of declaring unilateral independence.

But financial markets might need to continue putting up with

secessionist noise as Mas

tries to extract fiscal concessions out of Madrid following the election.